Coming out of COVID, the manufacturing industry experienced a rebound fueled by pent-up demand, low interest rates, and a temporarily booming economy. However, supply chain disruptions and labor shortages began driving costs higher. Over the past two years, surging inflation has led to rising interest rates, reduced investment, and softened demand in certain sectors. Despite these challenges, early signs suggest the industry may be poised for another shift toward growth.

According to The CMO Survey1, optimism in the U.S. economy among manufacturing marketers has climbed into the mid-60s (on a scale of 1 to 100, with 100 being the highest). For context, this same group reported an optimism level of 57.3 in March 2023. Over the past decade, the lowest recorded optimism was 55.2 in June 2020, while the highest was 73.2 in August 2021.

With rising optimism and the tailwinds of an improving economic environment, enthusiasm for increased investment and growth is strengthening. This positive outlook inspired us to survey marketers and C-suite executives in the manufacturing industry to better understand their marketing efforts - particularly digital marketing. We explored what's working, the challenges they face, and how they leverage AI and external support to drive their initiatives forward.

Below, we present the results, key takeaways, and insights from our survey, which gathered responses from 114 U.S.-based manufacturers.

*Side note: For anyone who loves data, The CMO Survey is outstanding. Since 2008, the survey partners (Deloitte, Duke Fuqua, American Marketing Association) have surveyed senior marketing leaders 2x per year with a consistent set of questions. The data is dense, and the studies are 150+ pages, but if you have the time to sift through, seeing the trends in leadership sentiment, marketing priorities, and budget allocations is very interesting. All the data is broken out by company size, business model, and industry. See our sources section at the bottom of the page for a link to the surveys.

Respondents

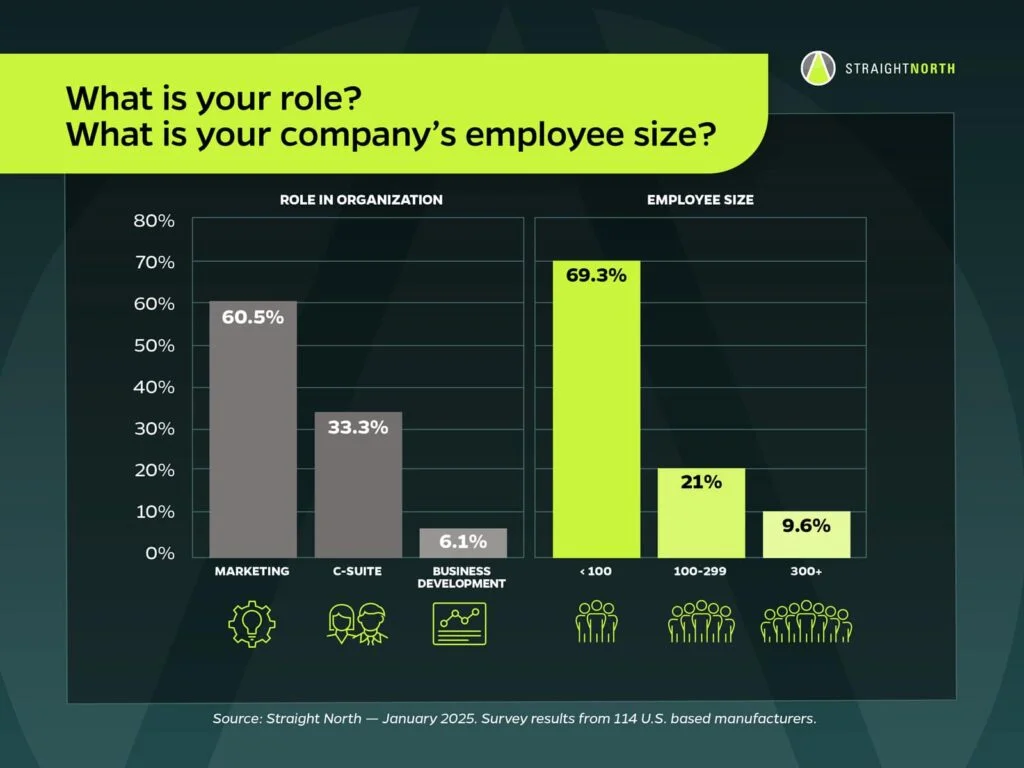

Before diving into the data, let's review the demographics of the respondent group.

Approximately 60% of respondents are marketers, 33% are C-Suite executives, and the remaining participants are in business development.

The majority - 70% of respondents - represented manufacturers with fewer than 100 employees.

AI and People (Internal and External)

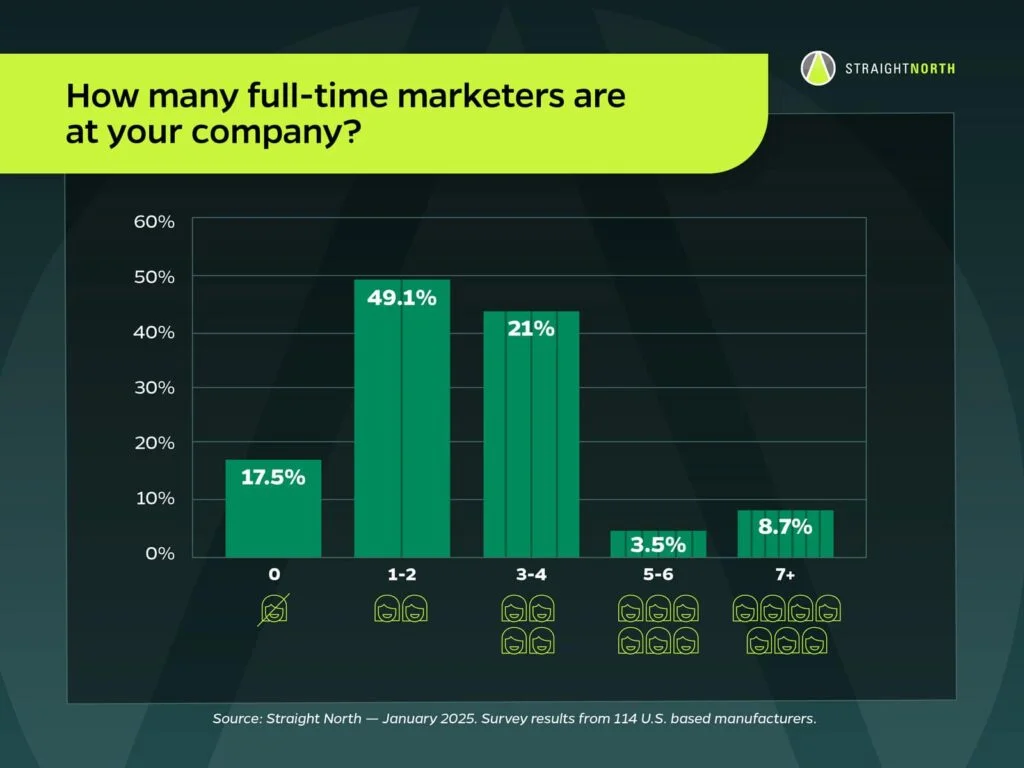

About 50% of respondents reported having 1-2 full-time marketers, followed by 21% with 3-4 full-time marketers.

As expected, a strong correlation exists between company size and the number of in-house marketers.

Among the respondents, marketers make up approximately 2% of the employee base, compared to an estimated 5% in other industries.

What stood out most to me was the number of companies with zero in-house marketers - 18%. Considering that 60% of respondents were marketers, this indicates their companies have at least one full-time marketer. Surprisingly, over half of the C-Suite respondents reported having no full-time marketers.

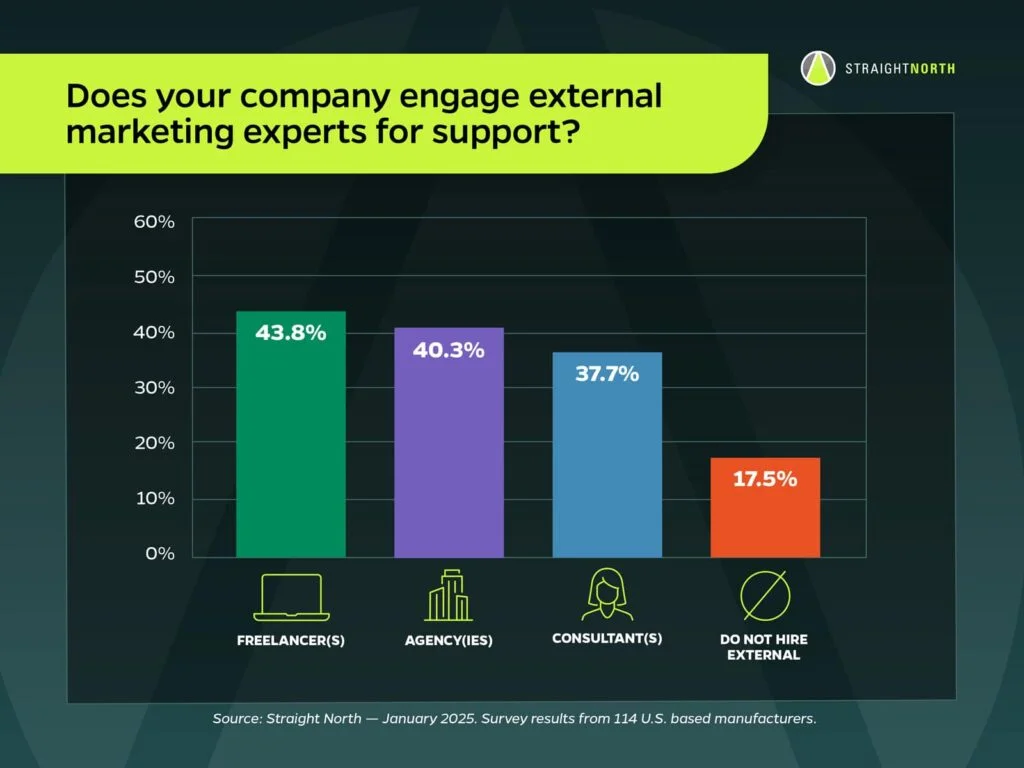

I found the balance in the responses fascinating - there is no clear consensus. Businesses are leveraging the external resources that best align with their unique needs and strategies.

For those that engage external support, most partner with at least two types of external groups.

Nearly all companies that do not hire external experts are small businesses with fewer than 50 employees and 1-2 full-time in-house marketers.

Business leaders across industries and functions are exploring how they can leverage AI to improve the quality and efficiency of their business practices. According to a 2024 McKinsey study2, 72% of businesses have adopted AI in at least one business function - up from 55% in 2023.

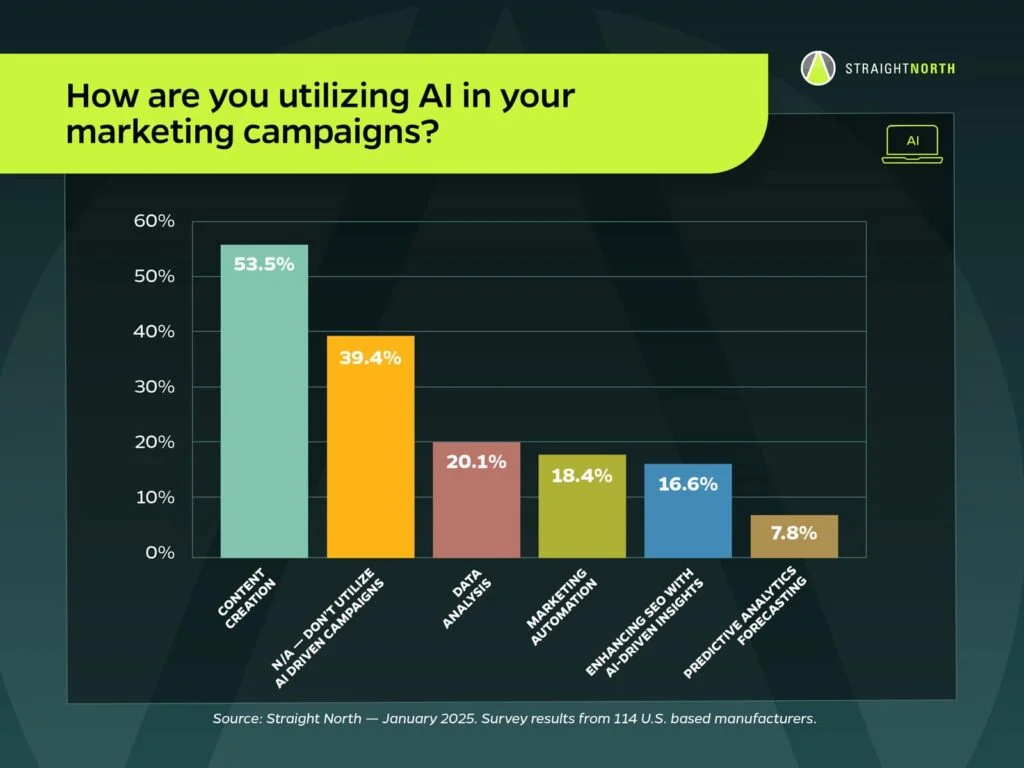

Given that manufacturers typically operate with leaner marketing departments, we aimed to understand how frequently and in what ways they are utilizing AI to support their efforts.

Among respondents, 60% reported using AI in their marketing initiatives, with the most popular use case being, unsurprisingly, content creation (84% that utilize AI use it for content creation).

The previously mentioned McKinsey study found that only 34% of businesses utilize AI in marketing and sales. This suggests one of two possibilities: Manufacturing marketers may be leading the way in AI adoption, or the pace of AI adoption is accelerating even faster than before. The McKinsey study was conducted just six months ago.

On the other hand, 40% of respondents reported not using AI. As large language models (LLMs) continue to improve and more practical use cases emerge, this number will likely decline over time.

On Which Channels are Marketers Focused and What's Working

I love this - it tells the exact story I'd expect. No marketing silver bullet exists in today's world. That's why a comprehensive digital marketing strategy is more critical than ever. Every prospect's buying journey is unique, and the better you can accommodate their journey, the stronger your results will be.

That said, I don't believe businesses need to market everywhere, all the time, or sacrifice quality for quantity. There's a prudent way to expand your strategy. But relying on just one or two channels not only creates excessive risk (trust me, I've learned this firsthand) but also significantly limits your ability to connect with your target audience in the ways they prefer to engage.

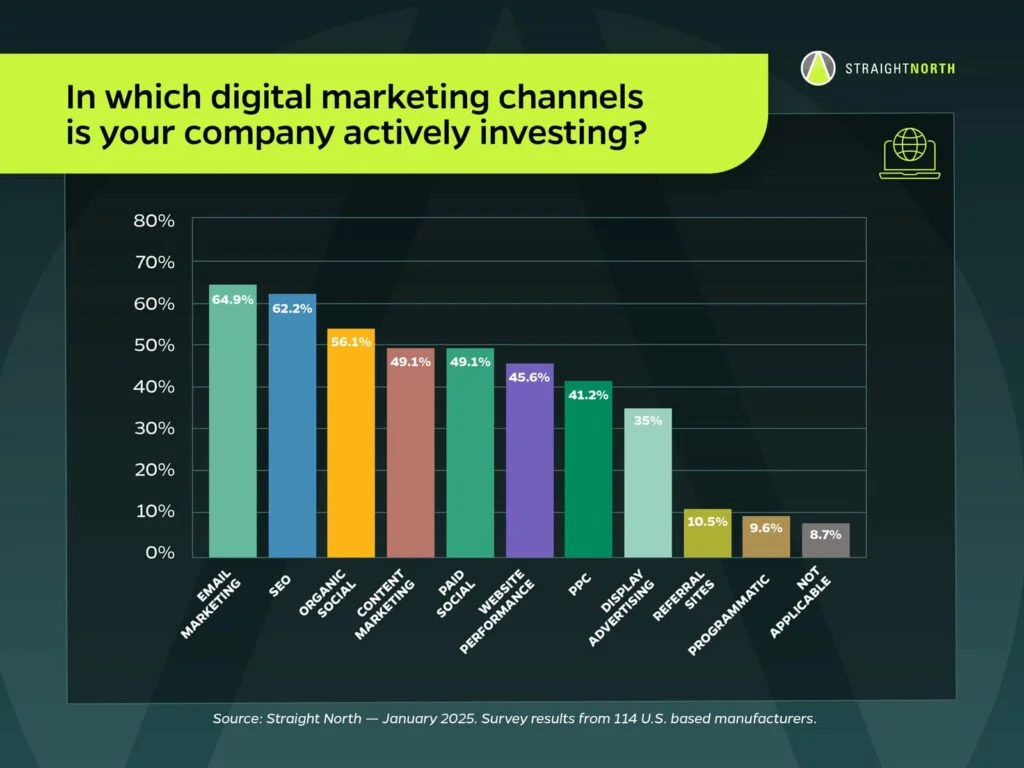

Regarding the data: Email Marketing leads the way, with 65% of respondents investing in that channel. SEO comes in second, with 62% of manufacturers allocating resources to it.

On average, businesses invest in four channels, though the most frequent response was six - 20% of businesses reported investing in six channels. Notably, a strong correlation exists between the number of marketers and the number of channels. For example, organizations with 1-2 marketers typically invest in four channels, while those with 5+ marketers average seven channels. This is both logical and expected.

Interestingly, 10% of manufacturers report no investment in digital marketing.

I acknowledge that success is multi-faceted. Does it mean which channel generates the best leads? The most leads? The cheapest leads? These are valid questions, but for simplicity, we left it up to the respondent's interpretation.

The leader is SEO, with 20% of manufacturers reporting it as their most successful digital marketing channel. Paid Social comes in second at 16%, followed by Email at 12%, and PPC at 11%.

Like many other channels, SEO presents its own set of challenges (which we'll explore further below). However, despite these hurdles, it consistently delivers results for manufacturers.

Challenges

I promise, I'm not the type of person to say, “I knew it” or “I told you so” (though my wife might disagree 🤔), but… I knew it! Of course, demonstrating return on investment (ROI) is the biggest challenge.

For those facing this issue, several reasons are likely. Some may lack proper CRM tools or MarTech systems. Others may struggle with attribution (more on that later) or have difficulty connecting the dots between marketing efforts and sales outcomes. Even with the right tools in place, demonstrating ROI for an individual channel is nearly impossible in today's multi-channel marketing landscape.

Refer back to our earlier question about the number of channels. When a business invests in four, five, or even six or more channels, how do you determine which channel contributed most to the buyer's journey? Sure, some cases are clear, but more often than not, it's a combination of channels working together. When a lead comes in, who gets the credit? Is it the last channel that brought the prospect to your site? The first channel? Or do you assign credit to all the channels that touched the buyer along the way? And how do you account for zero-click searches when your brand appears in an LLM or SGE result? It's a complicated process, and that's assuming your tracking systems tell the whole story - something that, increasingly, isn't the case.

For those struggling with this challenge, I wish I could offer a definitive solution, but I don't have one. In my opinion, consistency in your attribution methodology, staying focused on your core KPIs (e.g. leads, closes, contract revenue, etc.), and trusting your instincts are key. Any good marketer has a solid idea of what's working and what isn't. However, convincing executive leadership and stakeholders with a “just trust me” approach? That's a whole different challenge.

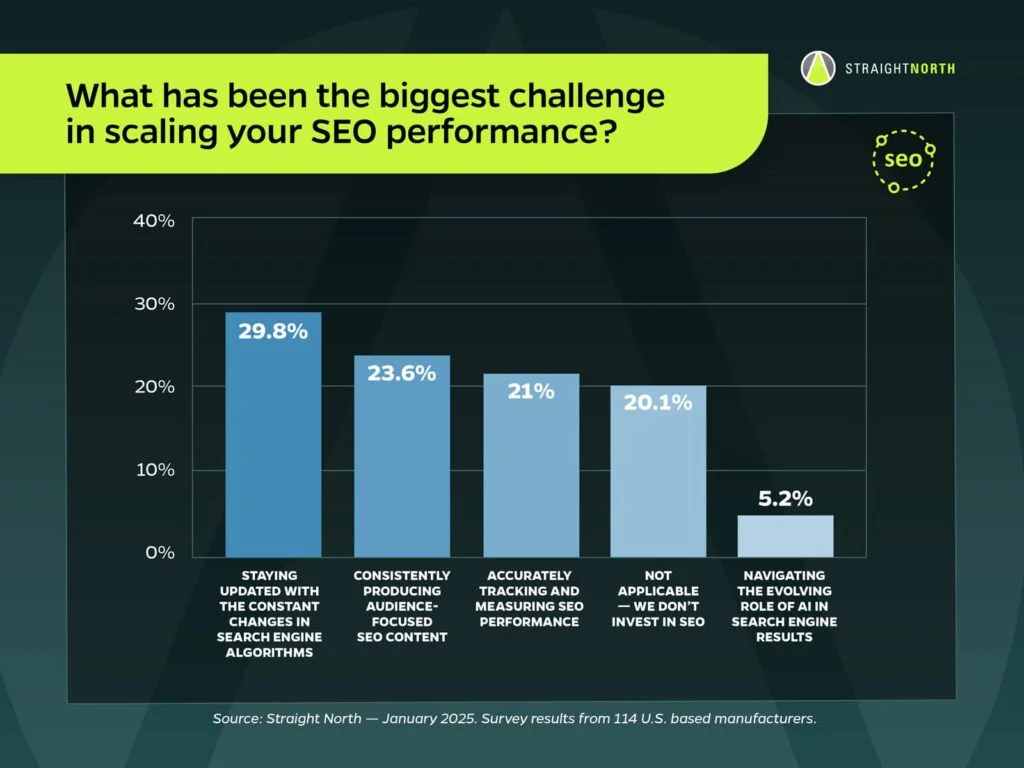

Since 2021, Google has averaged over 10 algorithm updates per year - 14 in 2021, 10 in 2022, 9 in 2023, and 9 in 20243. It's no surprise that a leading 30% of respondents cite staying updated with changes to search engine algorithms as their SEO biggest challenge.

The second most significant challenge is producing content that resonates with both the audience and the search engines.

Surprisingly, in third place, 20% of respondents identified their biggest challenge as accurately tracking and measuring SEO performance. Based on responses regarding overall digital marketing challenges, I would have expected this to rank higher.

In fourth place (excluding those who don't invest in SEO) is navigating the evolving role of AI in search results. If Google continues to expand SGE's presence on results pages and as more people use LLMs (like ChatGPT) as search tools, I anticipate this will climb higher on the list of challenges. Furthermore, as SGE and LLMs become more prominent, challenges related to content production (creating content that resonates with audiences, search engines, and LLMs) and tracking results (particularly for zero-click searches) are likely to increase.

When a channel is as effective as SEO, challenges are inevitable. If there weren't any, it probably wouldn't be as valuable as a marketing channel.

Marketing Investment

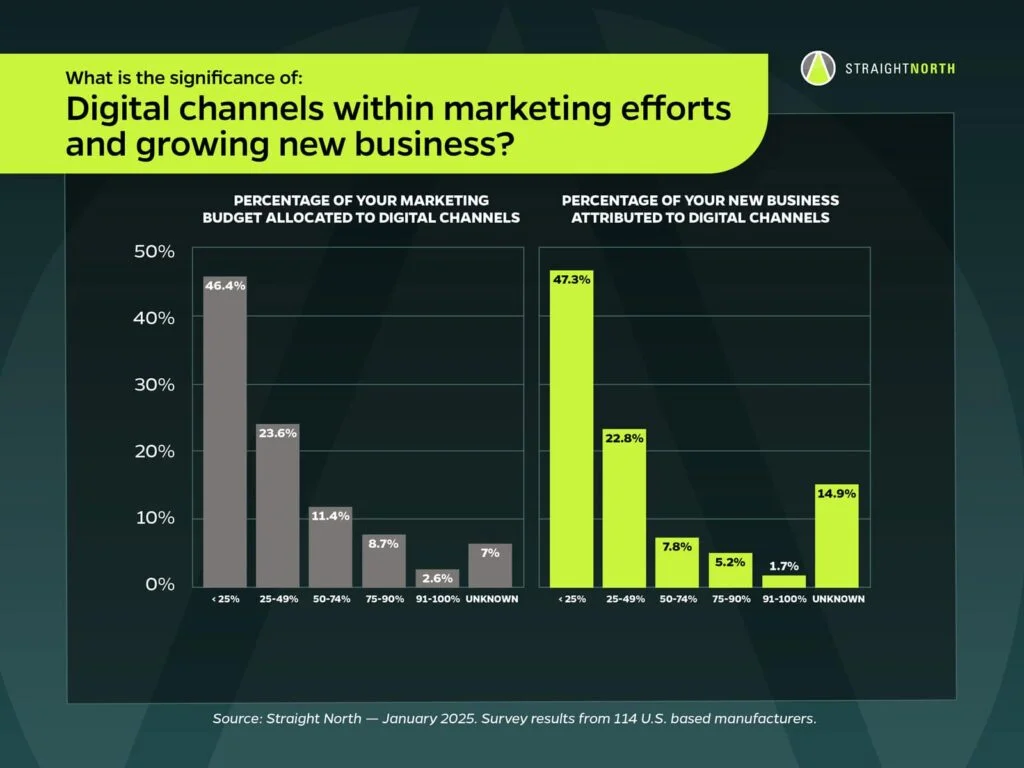

These two questions explored the role and impact digital marketing has on respondents' overall marketing investment and new business generation. As shown in the graphs, the trends are almost identical: Companies that allocate a smaller percentage of their marketing budgets to digital channels generate less new business from those channels. Conversely, as digital marketing investments increase, so does the proportion of new business attributed to digital efforts. While this isn't an earth-shattering revelation, seeing how consistently the data supports this relationship is fascinating.

Admittedly, I'm a bit biased given that Straight North is a digital marketing agency, but these findings underscore the growth opportunity manufacturers have by increasing their digital marketing investments.

Similarly, The CMO Survey1 highlighted some compelling insights from previous surveys. In 2022 and 2023, manufacturers reported that their digital marketing investments exceeded their non-digital investments, with a split of roughly 55% digital to 45% non-digital. Additionally, between 2021 and 2024, respondents reported an average annual increase of ~11% in digital marketing investments, compared to a modest ~1.5% annual increase in overall marketing budgets. This data clearly illustrates the ongoing shift from non-digital to digital marketing.

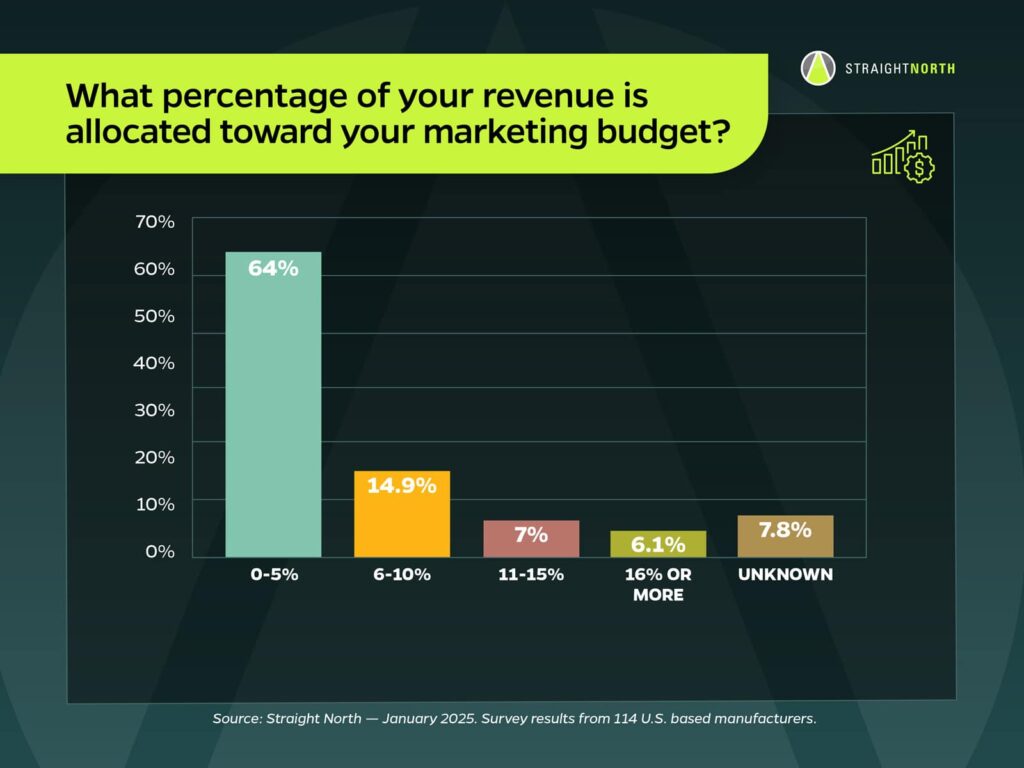

The final question focused on a timeless topic: How much is your company investing in marketing as a percentage of revenue? But perhaps the better question is, how much should you? As a business owner, I find this question fascinating because my partners and I wrestle with it constantly.

Over 60% of respondents reported allocating 0-5% of their revenue to marketing. There appears to be a modest correlation - though perhaps causation - between marketing investment and company size: the higher the investment (as a percentage of revenue), the larger the company.

Wrap up and thanks.

We appreciate everyone who participated in the survey. We found the respondent data very insightful - we hope you did too.

If you have any questions or need assistance navigating the digital marketing landscape and addressing your challenges, please don't hesitate to reach out to Straight North.